Understanding roof damage and insurance claims can feel overwhelming when you're facing unexpected repairs after severe weather strikes your property. Whether you're dealing with hail damage, wind-related issues, or other roofing problems, knowing how to navigate the insurance claims process effectively can save you thousands of dollars and significant stress. This comprehensive guide walks you through everything you need to know about documenting damage, filing claims, working with adjusters, and ensuring you receive fair compensation for your roofing repairs or replacement.

Understanding What Insurance Covers for Roof Damage

Homeowners insurance policies typically cover sudden and accidental roof damage, but the specifics vary significantly based on your policy type and coverage limits. Most standard policies protect against damage from wind, hail, fire, falling objects, and vandalism. However, understanding the nuances of your coverage is essential before filing a claim.

Covered Perils vs. Exclusions

Insurance companies distinguish between covered perils and exclusions when evaluating roof damage and insurance claims. Covered perils generally include:

- Storm damage from wind, hail, or lightning strikes

- Fire damage including damage from nearby fires

- Falling objects such as trees, branches, or debris

- Vandalism or malicious mischief

- Weight of snow or ice in applicable regions

Conversely, most policies exclude damage from:

- Normal wear and tear or aging

- Lack of maintenance

- Gradual deterioration

- Mechanical breakdown

- Pre-existing conditions

American Family Insurance provides detailed information about which types of roof damage are typically covered under homeowners policies. Understanding these distinctions helps you determine whether your specific situation warrants filing a claim.

Age and Coverage Considerations

The age of your roof significantly impacts how insurers handle claims. Many insurance companies use Actual Cash Value (ACV) for roofs older than 10-15 years, meaning they factor in depreciation when calculating payouts. Newer roofs typically qualify for Replacement Cost Coverage (RCC), which covers the full cost of replacement without depreciation.

| Coverage Type | How It Works | Best For |

|---|---|---|

| Actual Cash Value | Pays replacement cost minus depreciation | Older roofs (15+ years) |

| Replacement Cost | Pays full replacement cost without depreciation | Newer roofs (under 15 years) |

| Extended Replacement Cost | Pays above policy limits if costs exceed estimates | High-value properties |

| Guaranteed Replacement Cost | Pays whatever it costs to replace | Premium policies |

Documenting Roof Damage Properly

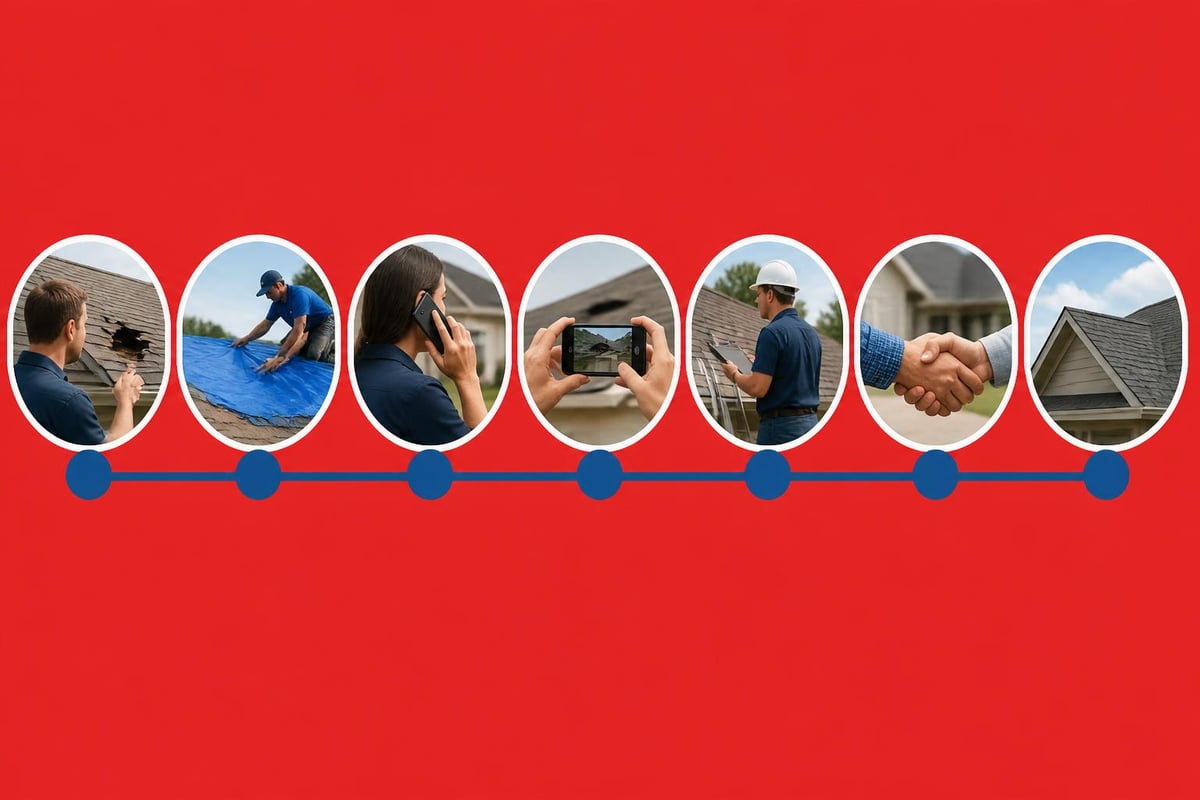

Proper documentation forms the foundation of successful roof damage and insurance claims. The more thorough your documentation, the stronger your position when negotiating with insurance adjusters. Begin documenting immediately after discovering damage, but prioritize safety over rushing onto a potentially compromised roof structure.

Initial Assessment Steps

Start by conducting a ground-level inspection using binoculars to spot obvious damage like missing shingles, dented vents, or damaged flashing. Take wide-angle photos showing the entire roof and close-up shots of specific damage areas. Document the date, time, and weather conditions when you discovered the damage.

Professional roofing contractors like those offering storm damage repair services can provide comprehensive inspections that identify damage not visible from the ground. Their expertise ensures nothing gets overlooked during the documentation process.

Creating a Damage Inventory

Compile a detailed inventory that includes:

- Photographic evidence from multiple angles and distances

- Written descriptions of each damaged area

- Measurements of affected sections

- Previous maintenance records proving proper upkeep

- Professional inspection reports from licensed contractors

Keep all documentation organized in both digital and physical formats. Cloud storage provides backup protection while physical copies serve as immediate reference during adjuster meetings.

The Claims Filing Process

Filing roof damage and insurance claims requires attention to detail and adherence to specific timelines. Most policies require notification within a reasonable timeframe, typically 48-72 hours after discovering damage, though "reasonable" varies by policy and circumstances.

Immediate Steps After Damage

Contact your insurance company immediately to report the damage and initiate the claims process. Request claim number assignment and clarification on next steps. Ask about emergency repair coverage, as most policies allow temporary repairs to prevent further damage.

The process for filing hail damage claims outlined by Nationwide emphasizes the importance of acting quickly while maintaining detailed records. Document all conversations with your insurer, including representative names, dates, and discussion summaries.

Working With Your Insurance Adjuster

Insurance adjusters evaluate damage and determine claim payouts. When the adjuster schedules their inspection, ensure you or your contractor representative is present. This allows real-time discussion of damage and prevents overlooked issues.

Prepare for the adjuster visit by:

- Having all documentation readily available

- Highlighting specific damage areas

- Providing contractor estimates for comparison

- Asking questions about coverage and depreciation

- Requesting written explanation of any denied items

Consider having a professional roofing contractor present during the inspection. Their expertise can identify damage the adjuster might miss and provide technical context that supports your claim.

Maximizing Your Insurance Settlement

Understanding how to maximize your settlement while maintaining honesty and integrity ensures you receive fair compensation for legitimate damage. This doesn't mean inflating claims but rather ensuring every covered item receives appropriate consideration.

Getting Multiple Estimates

Obtain at least three detailed estimates from licensed, insured roofing contractors. These estimates should itemize materials, labor, and associated costs. Comparative estimates demonstrate market rates and strengthen your position if the adjuster's assessment seems low.

Quality contractors provide transparent breakdowns showing:

- Material specifications including manufacturer and grade

- Labor costs itemized by task

- Permit fees and regulatory compliance costs

- Disposal expenses for old materials

- Warranty information for materials and workmanship

When evaluating whether to file a claim, consider the potential long-term costs versus your deductible and possible premium increases. Minor damage costing slightly above your deductible may not justify filing if it triggers rate hikes.

Understanding Depreciation and Recoverable Depreciation

Many policies pay claims in two phases. The initial payment represents actual cash value (replacement cost minus depreciation). After completing repairs, you can recover the depreciation amount by submitting proof of completed work and paid invoices.

To recover depreciation:

- Complete all repairs using licensed contractors

- Obtain itemized, paid invoices

- Submit invoices to your insurance company

- Provide photos of completed work

- Request release of recoverable depreciation

Common Claim Denial Reasons and How to Appeal

Insurance companies deny roof damage and insurance claims for various reasons, but denials aren't necessarily final. Understanding common denial reasons helps you build stronger initial claims and prepare effective appeals when necessary.

Typical Denial Justifications

Insurers most frequently deny claims based on:

- Pre-existing damage or deferred maintenance

- Age-related deterioration versus storm damage

- Policy exclusions or coverage gaps

- Insufficient documentation of damage

- Missed filing deadlines or notification requirements

When facing denial, request a detailed written explanation citing specific policy language. This documentation proves essential for appeals or legal action.

The Appeals Process

Most insurance companies have formal appeals processes allowing you to challenge denials. Successful appeals typically require additional evidence addressing the denial reason.

| Appeal Element | Purpose | Key Components |

|---|---|---|

| Independent Inspection | Third-party verification | Licensed engineer or contractor report |

| Expert Opinion | Technical support | Professional assessment contradicting adjuster |

| Additional Documentation | Fill evidence gaps | Photos, videos, weather reports |

| Policy Review | Identify coverage | Legal interpretation of policy language |

Professional legal assistance may become necessary for complex disputes. In some cases, tax implications can arise from insurance settlements, particularly for commercial properties, and consulting with specialists like those at the Law Offices of Darrin T. Mish, P.A. can help navigate any financial complexities related to settlement proceeds.

Choosing the Right Roofing Contractor

Selecting a qualified contractor significantly impacts both claim success and repair quality. Insurance companies prefer working with licensed, insured professionals who provide detailed documentation and stand behind their work.

Essential Contractor Qualifications

Verify contractors possess:

- Valid licensing in your state and locality

- Comprehensive insurance including liability and workers' compensation

- Manufacturer certifications for materials they install

- Local references from recent similar projects

- Written warranties covering materials and workmanship

Your local roofers understand regional weather patterns, building codes, and insurance company expectations. This local expertise streamlines the claims process and ensures repairs meet all regulatory requirements.

Red Flags to Avoid

Steer clear of contractors who:

- Offer to waive your deductible

- Pressure immediate signing of contracts

- Request full payment upfront

- Lack proper licensing or insurance

- Promise to inflate claim amounts

These practices may seem beneficial initially but often lead to substandard work, claim complications, or even insurance fraud allegations.

Preventing Future Roof Damage

Proactive maintenance reduces future damage risk and strengthens your position should you need to file subsequent roof damage and insurance claims. Insurance companies favor policyholders who demonstrate consistent property care.

Regular Maintenance Schedule

Implement a maintenance program including:

- Biannual inspections in spring and fall

- Immediate minor repairs addressing small issues before they escalate

- Gutter cleaning preventing water backup and ice dams

- Ventilation checks ensuring proper attic airflow

- Tree trimming reducing falling branch risks

Understanding proper attic ventilation helps prevent moisture-related damage that insurance typically doesn't cover. Proper ventilation extends roof lifespan and prevents premature deterioration.

Documentation for Future Claims

Maintain ongoing records including:

- Annual inspection reports from licensed contractors

- Receipts for all repairs and maintenance

- Photos documenting roof condition over time

- Warranty information for materials and installations

- Correspondence with insurance company about coverage

This documentation trail proves proper maintenance if you file future claims, countering potential denial arguments based on neglect.

Special Considerations for Commercial Properties

Commercial roof damage and insurance claims involve additional complexities compared to residential properties. Commercial roofing systems like modified bitumen require specialized knowledge for proper damage assessment and repair.

Business Interruption Coverage

Commercial policies may include business interruption coverage compensating for revenue loss during repairs. This coverage requires:

- Detailed financial records proving normal revenue patterns

- Documentation of closure period directly related to roof damage

- Evidence of repair necessity preventing business operations

- Professional accounting of actual losses incurred

Different Coverage Standards

Commercial policies often feature higher deductibles, different depreciation schedules, and more complex coverage limits than residential policies. Working with contractors experienced in commercial claims ensures proper handling of these nuances.

Working With Great Roofing on Your Claim

Professional roofing contractors serve as invaluable advocates throughout the claims process. Their expertise in both roofing systems and insurance procedures helps homeowners and business owners navigate complex situations confidently.

Experienced contractors provide:

- Accurate damage assessments identifying all covered issues

- Detailed estimates supporting fair settlement amounts

- Insurance company communication using industry terminology

- Quality repairs meeting or exceeding code requirements

- Warranty protection for materials and workmanship

Understanding materials options, such as exploring the best metal roofing materials for your climate, helps make informed decisions about replacement versus repair during the claims process.

Timing and Seasonal Considerations

The timing of your claim filing and repair scheduling affects both process efficiency and final costs. Seasonal factors influence material availability, contractor scheduling, and even adjuster responsiveness.

Peak Season vs. Off-Season Claims

Storm seasons typically see claim volume spikes, resulting in:

- Longer adjuster response times

- Extended contractor wait periods

- Potential material shortages

- Higher temporary repair costs

Filing during off-peak periods may accelerate processing, though you can't always control when damage occurs. Emergency repairs become critical when winter weather threatens further damage to compromised roofing systems.

Weather Windows for Repairs

Most roofing work requires dry conditions and moderate temperatures. Plan repair timing considering:

- Temperature requirements for shingle adhesion and sealant curing

- Precipitation forecasts allowing adequate dry periods

- Daylight hours for safe, quality workmanship

- Material storage protecting supplies from weather damage

Navigating roof damage and insurance claims successfully requires understanding coverage details, documenting damage thoroughly, and working with experienced professionals who advocate for your interests. By following the steps outlined in this guide and maintaining proactive roof care, you position yourself for fair settlements when unexpected damage occurs. Whether you're dealing with storm damage, need professional assessment, or require expert repairs, Great Roofing provides the expertise and integrity to guide you through every step of the insurance claims process while delivering superior roofing solutions for your Joliet-area property.